It’s instructive to look at Tier1 ISPs separate from their Lower Tier counterparts.

Tier 1 Internet providers provide the backbone of the Internet. They provide traffic to all other Internet providers, but not to end users. They connect to each other for mutual benefit, through mutual agreements.

Tier 2 ISP connect to Tier1 ISPs, through bandwidth transit purchase agreements and some peer relationships with other Tier 2 ISPs.

Tier 3 ISPs provide the last mile connection to business and residential customers. Again, connection to the parent Tiers are fee based. The boundary between Tier 2 & 3 can get a little blurry.

The growth of CDNs is pushing the content delivery out towards the Tier 2 Exchange Points, and Tier 3 ISPs. To a degree, this offsets bandwidth expenditures that would otherwise be incurred, but likely raises other operational costs material to operating the co-located hardware.

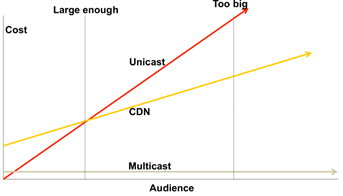

To put Centralized Unicast, CDN Unicast, and Multicast into comparative economic perspective, I’ve borrowed a graphic from my colleague Lenny Giuliano at Juniper Networks. (Giuliano, 2014)

Centralized Unicast cost scales linearly across audience size. However, at some large audience size, the costs become intolerable.

Comparatively, CDN has a greater upfront cost. Fortunately, at some “Large enough” audience size, the CDN costs drop below that of Centralized Unicast.

Multicast has a low fixed cost, and it tends to remain low, compared to the Unicast alternatives.

As the proposed Multicast methods so significantly relieve bandwidth burden, CSP might be inclined to reverse the trend towards greater edge server deployment. They might choose to centralize the many fewer Multicast servers, lessening the administrative complexities of CDN operation.